Accounting policy

Current income tax

Current income tax assets and liabilities are measured at the amount that is expected to be paid to or recovered

from the tax authorities. The current and deferred income tax is calculated based on tax rates and tax laws that

have been enacted or substantively enacted, in the countries where the Group operates and generates taxable

income. Management periodically evaluates positions taken in the tax returns with respect to situations in

which applicable tax regulations are subject to interpretation and establishes provisions where appropriate.

Deferred tax

Deferred tax assets and deferred tax liabilities are calculated on all differences between the book value and

tax value of assets and liabilities. Deferred tax assets and deferred tax liabilities are recognised at their nominal

value and classified as non-current liabilities and non-current assets in the balance sheet. Deferred tax liabilities

and deferred tax assets are offset as far as possible as permitted by taxation legislation and regulations.

Deferred tax assets are recognised for all unused tax losses and temporary differences to the extent that it is

probable that taxable profit will be available against which losses and temporary differences can be utilised.

Estimate and judgement

Uncertainties exist with respect to determining the Group’s deferred tax assets and deferred tax liabilities.

Significant management judgement is required to determine the amount of deferred tax assets that can be

recognised, based upon the likely timing and level of future taxable profits, together with future tax planning

strategies.

The Group is subject to income taxes in numerous jurisdictions, and judgement is involved when determining

the taxable amounts. Tax authorities in different jurisdictions may challenge the calculation of taxes payable

from prior periods. Management judgement is required when assessing valuation of unused losses, tax credits

and other deferred tax assets. The recoverability is assessed by estimating taxable profits in future years taking

into consideration expected changes in temporary differences.

Indirect tax regimes are complex in many jurisdictions. The basis for such taxes may differ from actual

transaction prices. In some jurisdictions, including Brazil, significant credit amounts are generated for use

against future indirect and/or income tax payments. The value of such credits depends on future taxable

income. Economic conditions and tax regulations may change and lead to a different conclusion regarding

recoverability. Tax authorities may challenge Jotun’s calculation of indirect taxes and credits from prior periods.

Such processes may lead to changes to prior periods’ operating expenses to be recognised in the period of

change.

Back to contents >

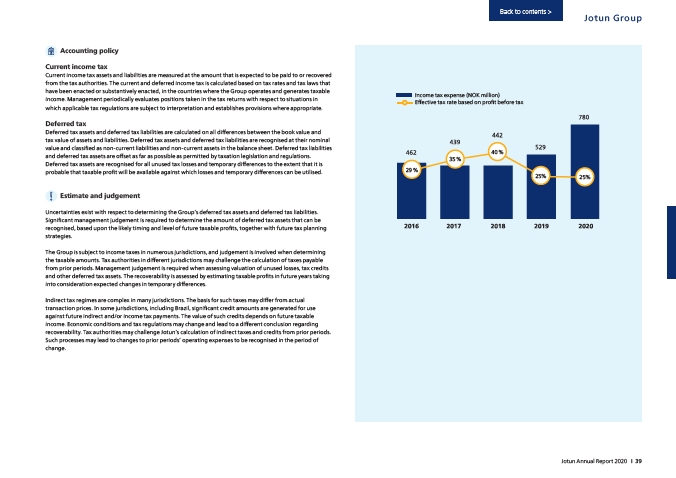

Income tax expense (NOK million)

Effective tax rate based on profit before tax

29 %

35 %

40 %

Jotun Group

25% 25%

Jotun Annual Report 2020 I 39